Tax Talk is a regular series written by FSL’s tax expert, Alex Ranahan. Alex has nearly ten years’ experience as a tax adviser and analyst. He is accredited by The Association of Taxation Technicians. Alex’s Tax Talks are on general topics and are not tax or financial advice. If you are unsure of the tax treatment of a transaction, we encourage you to seek the appropriate tax advice.

One danger with a blog that runs monthly is that some juicy, relevant topics can come and go in the public’s attention before we’ve even planned the next post. On the other hand, a view taken when the dust has settled on an issue can be more holistic. Whilst we will not comment directly on the story which dominated the news a few weeks ago, we hope to provide a useful guide to the principles underpinning these two regimes. In some cases, we have simplified things quite a bit so as always do not take this blog as tax or financial advice.

It is fairly common sense that a country should only be able to take money off you in the form of tax if you live there, you do business such as buying or selling goods and services there or have some connection to it like work or owning property. For example, I have never set foot in the United States and therefore would be rather miffed if a letter from the Internal Revenue Service came through my door suggesting I owed them some of my income.

Residence rules

The idea that the country in which you live is where you pay tax is known as tax residence. Different countries have different ways of deciding if you are tax resident. Spain looks at whether you have either spent more than half the calendar year (183 days) there or have most of your economic interests based there, while New Zealand checks for either that 183 days again or if you have a permanent place to live there.

Until 2013, the UK used a mixture of the number of days physically here (a matter of fact) and the individual’s intentions (a matter of opinion and deduction) to decide if an individual was resident, and had the phrase ‘ordinarily resident’ to describe a person’s residence over the long term.

Since 6 April 2013 we have had the statutory residence test (SRT). The SRT provides a set of objective tests to determine, in order, whether someone is:

- Automatically not UK resident

- Automatically UK resident

- UK resident by circumstances (number of ‘ties’ to the UK)

For example, the first automatic overseas test states you are non-UK resident for the tax year if you were resident in the UK for at least one of the three previous tax years and you spend fewer than 16 days in the UK in the tax year. The first automatic UK test states that you are UK resident for the tax year if you spend – you guessed it – 183 days or more in the UK in the tax year.

It gets even more complicated if you arrive in or leave the UK partway through the tax year and need to study the split year rules, or if you live abroad for a short time before returning to the UK and need to look at the temporary non-residence rules – though we won’t examine these here.

Tax treatments

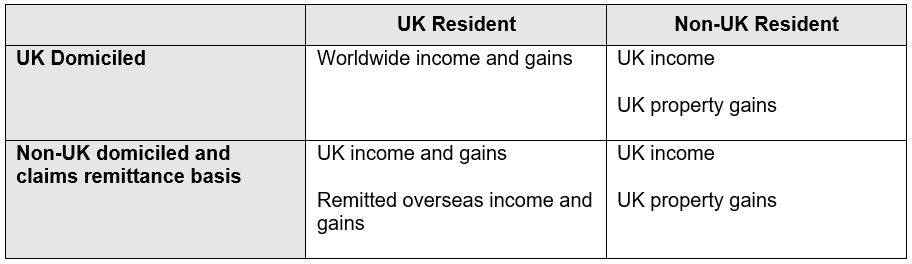

But how does this relate to one’s UK tax treatment? Looking at Income Tax and Capital Gains Tax only, you are taxed in the UK like so:

To be clear, the picture is more complicated than this. We have not touched on disregarded income or other areas of UK tax for non-residents as this blog is not a full review of the UK tax system for international individuals. But, as you can see, non-UK residents are treated essentially the same regardless of domicile, but a UK resident who is UK domiciled (in tax talk, that person is a UK ‘domiciliary’) is taxed very differently to a UK resident with a non-UK domicile.

A non-UK domiciliary who is UK resident is entitled – but not required – to claim the remittance basis of taxation, which allows them to pay UK tax on only their UK income and gains. They are only taxed on overseas income and gains if sums derived from overseas are transferred into the UK, or say, assets acquired using overseas money are physically brought into the UK. The act of bringing overseas amounts or assets into the UK is known as a remittance.

Remittance basis of taxation

A ‘non-dom’ is entitled to claim the remittance basis of tax for up to 15 years of UK residence out of the past 20 years. After 15 years they acquire a ‘deemed domicile’ in the UK and are taxed on their worldwide income and gains. At first the non-dom may claim the remittance basis by simply ticking the relevant box on their tax return, but if they have been UK resident for 7 out of the previous 9 years then they must pay £30,000 for the privilege. This rises to £60,000 if they have been UK resident for 12 out of the previous 14 years.

However, by claiming the remittance basis, the individual loses entitlement to certain reliefs such as the personal allowance for Income Tax and the annual exemption for capital gains tax (CGT). Given that the median household disposable income in 2021 was £31,400, most people will find that the personal allowance covers the bulk of their income and the remainder is only taxed at 20%. Claiming the remittance basis and losing their personal allowance would only be worthwhile if they also happen to have substantial overseas income/gains which – crucially – never enters the UK.

Having said this, the remittance basis applies automatically without any loss of personal allowance or annual exemption if the non-UK domiciliary’s income and gains are less than £2,000 and are not remitted to the UK.

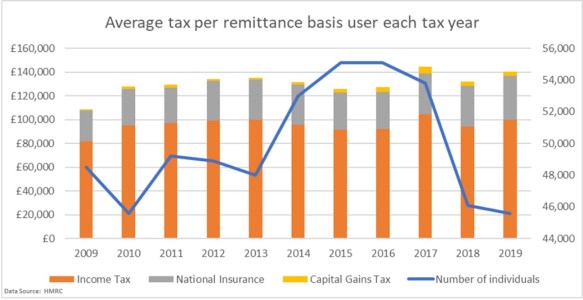

Provisional figures from HMRC show only 45,600 individuals claimed the remittance basis for the 2018/19 tax year, paying a total of £4.5 billion Income Tax, £171m CGT and £1.7 billion National Insurance. Of those remittance basis users, 1,400 paid the £30,000 remittance basis charge in 2018/19 while only 500 paid the £60,000 charge. This works out at an average tax bill of £140,000 per year for each non-dom who claims the remittance basis (see the graph below). This does not take into account the remittance basis charge, and of course does not consider other taxes such as VAT.

Researchers at the University of Warwick this year calculated that 0.3% of those earning less than £100,000 have claimed non-dom status. This supports the point that it is mostly those non-doms whose UK income and gains are great enough that they can afford to lose their allowances who will claim the remittance basis.

The future for non-doms

So where does that leave us? The press and the public have jumped on the story with the usual zeal, demanding a ‘fairer’ tax system. The Labour Party has announced that it will scrap non-dom status and replace it with a temporary UK resident scheme. But with the cost of living crisis, war in Ukraine and Downing Street parties pushing tax off the front pages, will the appetite for serious reform persist? This blog can’t answer that. But when it comes to UK investment we have seen the Government’s willingness to put investors first – see the Chancellor’s refusal to countenance a windfall tax or the new asset holding companies regime.

Overseas investors who come to the UK may claim the remittance basis at first, saving lots of tax in some cases, but when it comes to remitting more funds into the UK for investment they are discouraged by the tax charge they’ll be hit by for doing so. There are clearly conflicting policies here and it will take careful thought, and study of success stories in other countries, if the Government is to maintain the UK’s attractiveness to overseas investment without also attracting criticisms of an ‘unfair’ tax system.