Offshore funds are now common part of investors’ portfolios thanks to their increased availability on UK investment platforms. This has given advisers and their clients greater choice and diversification opportunities than ever before but there’s a growing – and potentially costly – problem hiding beneath the surface.

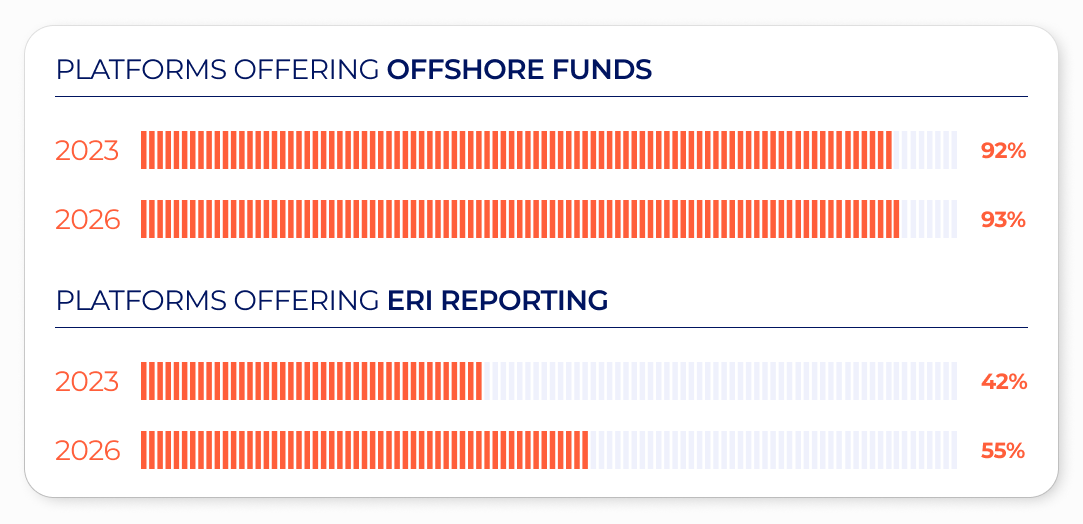

New research from tax software specialists Financial Software Ltd (FSL) and data management experts Raw Knowledge has revealed a worrying gap between tax reporting readiness on UK investment platforms and the availability of offshore funds.

Their research found that while 93% of platforms offer offshore funds, only 55% provide tools to support Excess Reportable Income (ERI) reporting. For advisers, this presents a growing operational burden and a serious tax compliance risk for their clients.

Misunderstood and Overlooked

ERI is the profit earned by an offshore reporting fund that is retain within the fund, rather than being distributed to investors. Even though investors do not directly receive this income, HMRC still treats it as having been earned for tax purposes. As result, the tax authority expects investors to declare ERI on their tax returns and pay income tax on the relevant amounts.

Failure to do so, or reporting inaccurate ERI information, could lead to penalties of up to 200% of the tax due, plus any interest and late payment penalties.

While ERI doesn’t impact every investor – just those with an offshore reporting fund held outside a tax-efficient wrapper like an ISA or SIPP – the increased demand for Model Portfolio Services (MPS) means more and more investors are being pulled into the ERI net.

The Growth in Offshore Funds

Research from Platforum shows assets under management across platform MPS solutions has nearly quadrupled over the past six years, rising 293%. Many of these MPS will contain offshore funds. In fact, data from the lang cat shows that almost two-third (61%) of the MPS ranges on its Analyser software include offshore funds. This means there’s a high likelihood that an investor holding one of these investments would need to report ERI information to HMRC, if they were to hold them within a General Investment Account.

Where platform support for ERI is lacking, this scenario could leave many advisers ill-equipped to accurately manage and report their clients’ tax liabilities.

Exchange Traded Funds (ETFs) – the fastest growing investment product in the UK, according a 2024 report by BlackRock – are a similar story, with just 11% of the funds offered by the UK’s largest ETF provider, iShares, being UK-domiciled.

Fragmented ERI Data Environment

Unfortunately for advisers and their clients, sourcing, calculating, and reporting ERI remains a challenge. At the heart of the issue is a fragmented and inconsistent data landscape.

There is no legal requirement for offshore reporting funds to publish their ERI information in a way that is easily accessible or easy-to-read for institutions or investors. The tax position of an offshore reporting fund only needs to be published somewhere. It could be deep on the fund’s website, located on a third-party webpage or contained within a 100-page PDF emailed to an investor.

This lack of structure often forces advisers and accountants into time-consuming manual searches – trawling fund factsheets or websites to find the right ERI information to file their clients’ tax returns. This creates significant operational burden for already stretched teams and increases the likelihood of errors and late fillings.

Complex Calculations and Reporting

Once the data has been sourced, the challenge for advisers doesn’t stop there. The process of reporting ERI introduces further complexities.

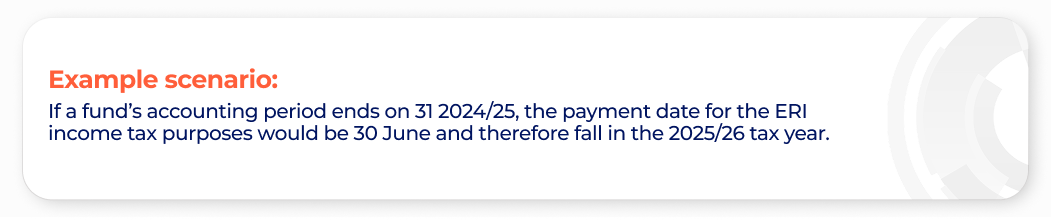

One of the key challenges is timing. By law, the payment date for ERI is always six months after the accounting period end-date for the company. The time lag can often lead to ERI crossing over two tax years, creating confusion when it comes to reporting, particularly where holdings are bought or sold within that six-month window.

Increasing HMRC Scrutiny

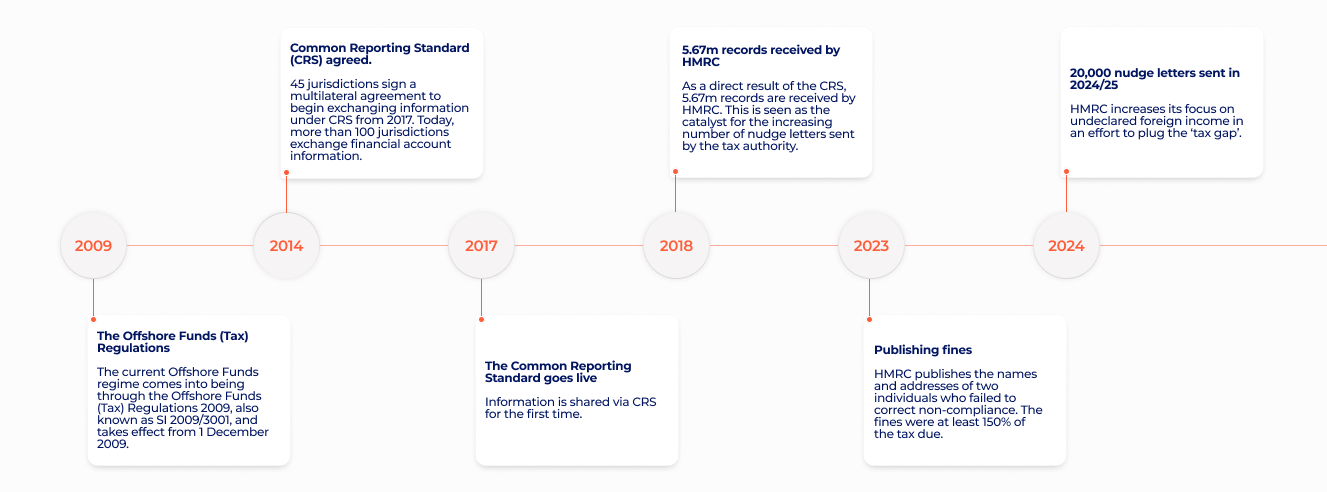

At the same time, HMRC is piling on the pressure. The tax authority sharpening its focus on overseas income as it looks to plug the UK’s ‘tax gap’ which is currently stands at an estimated £46.8 billion. It has issued around 20,000 letters to individuals in the 2024/25 tax year, specifically targeting undeclared foreign income.

These letters inform investors that HMRC know that they have investments, some of which contain offshore investments. Should enquiries then be opened, HMRC can start requesting extensive records for specific tax years – often these requests are sent to the investor directly, even when an accountant or advisers is in place. This can lead to some difficult and awkward conversations for advisers and their clients.

Consumer Duty Considerations

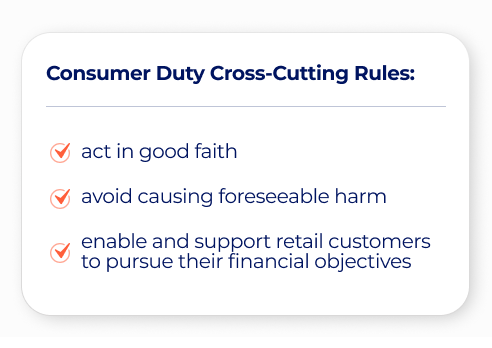

While it is ultimately the investor’s responsibility to ensure their tax returns are accurate and timely, under Consumer Duty, the UK Financial Conduct Authority want to see that a platform’s products and services have been designed to meet the needs of its target market. It can therefore be argued that by offering offshore funds to invest in while not being able to satisfy ERI reporting requirements, a platform would not be serving their target market effectively.

That being said, it is important to recognise that platforms are not legally required to provide this information to investors. Nonetheless, many platforms want to help but find themselves at the of mercy of a fragmented ERI data environment, resource constraints and a lack of specialist knowledge that makes consistent and accurate reporting a challenge.

This is where robust tax technology becomes essential to bridge the gap between the complex underlying data and the accurate, compliant reporting that both clients and regulators now expect.

The Need for Robust Tax Support

Offshore investing isn’t going away. If anything, it will only continue to grow as portfolios become more global and diversified. But it’s clear that platform support for ERI hasn’t kept pace with this reality.

Fragmented data, inconsistent availability and a lack of standardisation continue to create unnecessary complexity and increase the likelihood of errors, missed deadlines and unwelcome HMRC scrutiny. But better data alone will not fully address this challenge.

Advisers need access to robust, purpose-built tax technology capable of transforming these complex inputs into accurate, auditable outcomes. With the right systems in place, advisers can automate ERI calculations, apply the correct tax treatment, and ensure consistency across reporting, thereby reducing their operational burden while improving confidence in their results.

CGiX is designed to handle the intricacies of ERI, integrating seamlessly into wider tax workflows and ensuring that even the most complex scenarios are calculated and reported correctly.

As offshore fund exposure increases and regulatory expectations continue to rise, firms that rely on manual workarounds risk falling behind. Those that invest in scalable, accurate tax technology, however, will be far better positioned to manage risk, demonstrate compliance and deliver better outcomes for their clients.